只靠每天的架次數預測的Prophet與LSTM 模型

長短期記憶神經網路

當我們在理解一件事情的時候,通常不會每次都從頭開始學習,而是透過既有的知識與記憶來理解當下遇到的問題;事件的發生通常具有連續性,也就是一連串的因果關係,或是一個持續不斷變動的結果。在機器學習模型的發展中,引入這種遞歸 (recurrent) 的概念,是遞歸神經網路與其他神經網路模型 (如 CNN) 相比,較為創新的地方。長短期記憶模型則是改善了遞歸神經網路在長期記憶上的一些不足,因為其強大的辨識能力,可以有效的對上下文產生連結,現在已大量運用在自然語言理解 (例如語音轉文字,翻譯,產生手寫文字),圖像與影像辨識等應用。 在這邊我先不介紹LSTM的原理,因為這個專案並不是企圖改進LSTM的架構,大家只要知道他是具有理解時間關係的網路結構就可以了,既然prophet 和LSTM 都可以進行時間序列的處理 那我們就使用這兩個做個比較。

Meta Prophet 簡介:重點在於如何處理時間

Meta Prophet(全名:Facebook Prophet)是一款專門用於時間序列預測的開源工具,由 Facebook(Meta)開發。它以 Python 和 R 實作,設計目標是讓非專業統計人員也能輕鬆處理帶有季節性與節慶效應的時間序列數據。Prophet 被廣泛應用在營收、網站流量、銷售、需求等數據預測領域。

Prophet 的核心概念與架構

Prophet 將時間序列建模公式拆成三大部分: [ y(t) = g(t) + s(t) + h(t) + \epsilon_t ]

- g(t):trend(趨勢)

- s(t):seasonality(季節性成分)

- h(t):holidays(節日或特殊事件)

- ε:雜訊

Prophet 處理時間的關鍵特點

- 自動識別「時間」欄位

Prophet 要求資料有兩個欄位:

ds(datestamp,日期/時間)y(數值)

它會自動將 ds 欄位辨識為時間軸,並用它進行所有的分解與運算。

- 趨勢(Trend)建模

Prophet 支持兩種主要趨勢建模方式:

- 線性趨勢(可設定 changepoints 轉折點)

- logistic 增長(適合有上限的數據,如市場飽和)

Prophet 會在時間軸上自動尋找可能出現轉折(changepoints)的時刻,允許趨勢在不同時期改變成長率。 3. 週期/季節性(Seasonality)

Prophet 會自動加入年、週、日等週期性成分,透過傅立葉級數進行建模。你可以手動新增更多週期(如每月),或調整週期的強度。

- 節日/事件

你可以自訂「節日」時間清單(如農曆年、雙 11 等),Prophet 會自動在這些時間點上套用額外的預測效果(如特定天數的異常波動)。

- 處理缺漏值與不規則間距

Prophet 可直接處理缺漏資料與不等間隔的時間序列,不需手動補齊時間軸。

- 時間格式彈性

支援多種時間格式(日期、日期時間、timestamp),Prophet 會自動解析。

- 可擴展未來的時間軸

你只需告訴 Prophet 要預測幾天/幾週/幾個月後的數值,它會自動根據 trend 和 seasonality 外推時間序列。

Prophet 處理時間序列的步驟(Python 範例)

import pandas as pd

from prophet import Prophet

# 資料格式要求

# df 必須包含兩個欄位:ds(日期),y(數值)

df = pd.DataFrame({

'ds': pd.date_range('2023-01-01', periods=100),

'y': [ ... ] # 你的數值

})

# 建立模型

m = Prophet()

m.fit(df)

# 預測未來 30 天

future = m.make_future_dataframe(periods=30)

forecast = m.predict(future)

# 繪圖

fig = m.plot(forecast)

Prophet vs. LSTM:時間處理方式比較總結

| 處理特點 | Prophet | LSTM |

|---|---|---|

| 1. 時間格式解析 | 自動辨識 ds 欄位的時間格式(日期、datetime、timestamp 等) |

時間需手動轉換為連續數值或標準化後的時間特徵 |

| 2. 趨勢、季節性建模 | 內建趨勢與多重季節性建模邏輯(如年、週、日)可外加節日等事件效應 | 不會自動建模趨勢與季節性,需透過大量訓練數據學出時間模式 |

| 3. 缺漏資料處理 | 可直接處理不連續與缺漏資料,不需補齊時間軸 | 缺值需事先補齊,並要求固定間距的時間序列輸入 |

| 4. 未來預測方式 | 明確定義未來時間點,自動產生未來時間序列並套用模型外推 | 需遞迴地逐步預測下一時間點,常使用前一步預測作為下一步輸入 |

| 5. 時間粒度調整 | 可輕鬆切換日、週、月等粒度 | 時間粒度需在特徵工程階段預先設計 |

| 6. 複雜性與需求 | 適合小資料量、具明顯週期性與事件驅動的商業場景 | 適合大量數據、複雜長期依賴問題(如語音、股價等非週期性應用) |

|

||

|

||

| 算出來結果差不多 |

下面實戰

# -*- coding: utf-8 -*-

"""使用PROPHET 以及LSTM預測總架次數.ipynb

Automatically generated by Colab.

Original file is located at

https://colab.research.google.com/drive/1rRZQvGW2IOwRO1i1FZd_wGhz5iagkko6

"""

# @title

# 設定分割日 mday

mday = pd.to_datetime('2023-10-1')

# 建立訓練用 index 與驗證用 index

train_index = df2['ds'] < mday

test_index = df2['ds'] >= mday

# 分割輸入資料

x_train = df2[train_index]

x_test = df2[test_index]

# 分割日期資料(用於繪製圖形)

dates_test = df2['ds'][test_index]

"""### Read DATA"""

import pandas as pd

# 直接使用CSV檔案的URL

url = 'https://docs.google.com/spreadsheets/d/1hkHrnbn5oQPPHfBhiuieUzmVjsqW20XmRQWkhfWMomE/export?format=csv&id=1hkHrnbn5oQPPHfBhiuieUzmVjsqW20XmRQWkhfWMomE'

# 使用pandas讀取CSV

df = pd.read_csv(url)

# 顯示DataFrame的前幾行

df.head()

df.to_csv('calendar.csv', index=False)

import pandas as pd

# 讀取原始 CSV 檔案

df = pd.read_csv('/content/calender.csv')

# 確保日期格式正確

df['ds'] = pd.to_datetime(df['pla_aircraft_sorties'])

# 可以在這裡進行轉換,例如改欄位名稱、格式等

df.rename(columns={'pla_aircraft_sorties': 'value'}, inplace=True) # 轉為 Prophet 格式範例

df.rename(columns={'date': 'DATE'}, inplace=True) # 轉為 Prophet 格式範例

# 儲存為新的 CSV 檔案

df.to_csv('/content/output.csv', index=False)

import pandas as pd

from datetime import datetime

def convert_for_prophet(input_file, output_file):

df = pd.read_csv(input_file)

df.columns = df.columns.str.strip()

df['DATE'] = pd.to_datetime(df['DATE'])

prophet_df = pd.DataFrame()

prophet_df['ds'] = df['DATE']

prophet_df['value']=df['value']

prophet_df['ds'] = prophet_df['ds'].dt.strftime('%Y-%m-%d')

prophet_df = prophet_df.sort_values('ds')

prophet_df.to_csv(output_file, index=False)

print(f"\n Save File {output_file}")

print("\n Preview:")

print(prophet_df.head())

return prophet_df

input_file = 'output.csv'

output_file = 'DEXVZUS_out.csv'

prophet_df = convert_for_prophet(input_file, output_file)

!pip install prophet

# Quandl for financial analysis, pandas and numpy for data manipulation

# fbprophet for additive models, #pytrends for Google trend data

import pandas as pd

import numpy as np

import prophet

# matplotlib pyplot for plotting

import matplotlib.pyplot as plt

import matplotlib

# Class for analyzing and (attempting) to predict future prices

# Contains a number of visualizations and analysis methods

class Stocker():

# Initialization requires a ticker symbol

def __init__(self, price):

self.symbol = 'the '

s = price

stock = pd.DataFrame({'Date':s.index, 'y':s, 'ds':s.index, 'close':s,'open':s}, index=None)

if ('Adj. Close' not in stock.columns):

stock['Adj. Close'] = stock['close']

stock['Adj. Open'] = stock['open']

stock['y'] = stock['Adj. Close']

stock['Daily Change'] = stock['Adj. Close'] - stock['Adj. Open']

# Data assigned as class attribute

self.stock = stock.copy()

# Minimum and maximum date in range

self.min_date = min(stock['ds'])

self.max_date = max(stock['ds'])

# Find max and min prices and dates on which they occurred

self.max_price = np.max(self.stock['y'])

self.min_price = np.min(self.stock['y'])

self.min_price_date = self.stock[self.stock['y'] == self.min_price]['ds']

self.min_price_date = self.min_price_date[self.min_price_date.index[0]]

self.max_price_date = self.stock[self.stock['y'] == self.max_price]['ds']

self.max_price_date = self.max_price_date[self.max_price_date.index[0]]

# The starting price (starting with the opening price)

self.starting_price = float(self.stock['Adj. Open'].iloc[0])

# The most recent price

self.most_recent_price = float(self.stock['y'].iloc[len(self.stock) - 1])

# Whether or not to round dates

self.round_dates = True

# Number of years of data to train on

self.training_years = 3

# Prophet parameters

# Default prior from library

self.changepoint_prior_scale = 0.05

self.weekly_seasonality = False

self.daily_seasonality = False

self.monthly_seasonality = True

self.yearly_seasonality = True

self.changepoints = None

print('{} Stocker Initialized. Data covers {} to {}.'.format(self.symbol,

self.min_date,

self.max_date))

"""

Make sure start and end dates are in the range and can be

converted to pandas datetimes. Returns dates in the correct format

"""

def handle_dates(self, start_date, end_date):

# Default start and end date are the beginning and end of data

if start_date is None:

start_date = self.min_date

if end_date is None:

end_date = self.max_date

try:

# Convert to pandas datetime for indexing dataframe

start_date = pd.to_datetime(start_date)

end_date = pd.to_datetime(end_date)

except Exception as e:

print('Enter valid pandas date format.')

print(e)

return

valid_start = False

valid_end = False

# User will continue to enter dates until valid dates are met

while (not valid_start) & (not valid_end):

valid_end = True

valid_start = True

if end_date < start_date:

print('End Date must be later than start date.')

start_date = pd.to_datetime(input('Enter a new start date: '))

end_date= pd.to_datetime(input('Enter a new end date: '))

valid_end = False

valid_start = False

else:

if end_date > self.max_date:

print('End Date exceeds data range')

end_date= pd.to_datetime(input('Enter a new end date: '))

valid_end = False

if start_date < self.min_date:

print('Start Date is before date range')

start_date = pd.to_datetime(input('Enter a new start date: '))

valid_start = False

return start_date, end_date

"""

Return the dataframe trimmed to the specified range.

"""

def make_df(self, start_date, end_date, df=None):

# Default is to use the object stock data

if not df:

df = self.stock.copy()

start_date, end_date = self.handle_dates(start_date, end_date)

# keep track of whether the start and end dates are in the data

start_in = True

end_in = True

# If user wants to round dates (default behavior)

if self.round_dates:

# Record if start and end date are in df

if (start_date not in list(df['Date'])):

start_in = False

if (end_date not in list(df['Date'])):

end_in = False

# If both are not in dataframe, round both

if (not end_in) & (not start_in):

trim_df = df[(df['Date'] >= start_date) &

(df['Date'] <= end_date)]

else:

# If both are in dataframe, round neither

if (end_in) & (start_in):

trim_df = df[(df['Date'] >= start_date) &

(df['Date'] <= end_date)]

else:

# If only start is missing, round start

if (not start_in):

trim_df = df[(df['Date'] > start_date) &

(df['Date'] <= end_date)]

# If only end is imssing round end

elif (not end_in):

trim_df = df[(df['Date'] >= start_date) &

(df['Date'] < end_date)]

else:

valid_start = False

valid_end = False

while (not valid_start) & (not valid_end):

start_date, end_date = self.handle_dates(start_date, end_date)

# No round dates, if either data not in, print message and return

if (start_date in list(df['Date'])):

valid_start = True

if (end_date in list(df['Date'])):

valid_end = True

# Check to make sure dates are in the data

if (start_date not in list(df['Date'])):

print('Start Date not in data (either out of range or not a trading day.)')

start_date = pd.to_datetime(input(prompt='Enter a new start date: '))

elif (end_date not in list(df['Date'])):

print('End Date not in data (either out of range or not a trading day.)')

end_date = pd.to_datetime(input(prompt='Enter a new end date: ') )

# Dates are not rounded

trim_df = df[(df['Date'] >= start_date) &

(df['Date'] <= end_date)]

return trim_df

# Basic Historical Plots and Basic Statistics

def plot_stock(self, start_date=None, end_date=None, stats=['Adj. Close'], plot_type='basic'):

self.reset_plot()

if start_date is None:

start_date = self.min_date

if end_date is None:

end_date = self.max_date

stock_plot = self.make_df(start_date, end_date)

colors = ['r', 'b', 'g', 'y', 'c', 'm']

for i, stat in enumerate(stats):

stat_min = min(stock_plot[stat])

stat_max = max(stock_plot[stat])

stat_avg = np.mean(stock_plot[stat])

date_stat_min = stock_plot[stock_plot[stat] == stat_min]['Date']

date_stat_min = date_stat_min[date_stat_min.index[0]]

date_stat_max = stock_plot[stock_plot[stat] == stat_max]['Date']

date_stat_max = date_stat_max[date_stat_max.index[0]]

print('Maximum {} = {:.2f} on {}.'.format(stat, stat_max, date_stat_max))

print('Minimum {} = {:.2f} on {}.'.format(stat, stat_min, date_stat_min))

print('Current {} = {:.2f} on {}.\n'.format(stat, self.stock[stat].iloc[len(self.stock) - 1], self.max_date.date()))

# Percentage y-axis

if plot_type == 'pct':

# Simple Plot

plt.style.use('fivethirtyeight');

if stat == 'Daily Change':

plt.plot(stock_plot['Date'], 100 * stock_plot[stat],

color = colors[i], linewidth = 2.4, alpha = 0.9,

label = stat)

else:

plt.plot(stock_plot['Date'], 100 * (stock_plot[stat] - stat_avg) / stat_avg,

color = colors[i], linewidth = 2.4, alpha = 0.9,

label = stat)

plt.xlabel('Date'); plt.ylabel('Change Relative to Average (%)'); plt.title('%s Currency History' % self.symbol);

plt.legend(prop={'size':10})

plt.grid(color = 'k', alpha = 0.4);

# Stat y-axis

elif plot_type == 'basic':

plt.style.use('fivethirtyeight');

plt.plot(stock_plot['Date'], stock_plot[stat], color = colors[i], linewidth = 3, label = stat, alpha = 0.8)

plt.xlabel('Date'); plt.ylabel('US $'); plt.title('%s Currency History' % self.symbol);

plt.legend(prop={'size':10})

plt.grid(color = 'k', alpha = 0.4);

plt.show();

# Reset the plotting parameters to clear style formatting

# Not sure if this should be a static method

@staticmethod

def reset_plot():

# Restore default parameters

matplotlib.rcParams.update(matplotlib.rcParamsDefault)

# Adjust a few parameters to liking

matplotlib.rcParams['figure.figsize'] = (8, 5)

matplotlib.rcParams['axes.labelsize'] = 10

matplotlib.rcParams['xtick.labelsize'] = 8

matplotlib.rcParams['ytick.labelsize'] = 8

matplotlib.rcParams['axes.titlesize'] = 14

matplotlib.rcParams['text.color'] = 'k'

# Method to linearly interpolate prices on the weekends

def resample(self, dataframe):

# Change the index and resample at daily level

dataframe = dataframe.set_index('ds')

dataframe = dataframe.resample('D')

# Reset the index and interpolate nan values

dataframe = dataframe.reset_index(level=0)

dataframe = dataframe.interpolate()

return dataframe

# Remove weekends from a dataframe

def remove_weekends(self, dataframe):

# Reset index to use ix

dataframe = dataframe.reset_index(drop=True)

weekends = []

# Find all of the weekends

for i, date in enumerate(dataframe['ds']):

if (date.weekday()) == 5 | (date.weekday() == 6):

weekends.append(i)

# Drop the weekends

dataframe = dataframe.drop(weekends, axis=0)

return dataframe

# Calculate and plot profit from buying and holding shares for specified date range

def buy_and_hold(self, start_date=None, end_date=None, nshares=1):

self.reset_plot()

start_date, end_date = self.handle_dates(start_date, end_date)

# Find starting and ending price of stock

start_price = float(self.stock[self.stock['Date'] == start_date]['Adj. Open'])

end_price = float(self.stock[self.stock['Date'] == end_date]['Adj. Close'])

# Make a profit dataframe and calculate profit column

profits = self.make_df(start_date, end_date)

profits['hold_profit'] = nshares * (profits['Adj. Close'] - start_price)

# Total profit

total_hold_profit = nshares * (end_price - start_price)

print('{} Total buy and hold profit from {} to {} for {} shares = ${:.2f}'.format

(self.symbol, start_date, end_date, nshares, total_hold_profit))

# Plot the total profits

plt.style.use('dark_background')

# Location for number of profit

text_location = (end_date - pd.DateOffset(months = 1))

# Plot the profits over time

plt.plot(profits['Date'], profits['hold_profit'], 'b', linewidth = 3)

plt.ylabel('Profit ($)'); plt.xlabel('Date'); plt.title('Buy and Hold Profits for {} {} to {}'.format(

self.symbol, start_date, end_date))

# Display final value on graph

plt.text(x = text_location,

y = total_hold_profit + (total_hold_profit / 40),

s = '$%d' % total_hold_profit,

color = 'g' if total_hold_profit > 0 else 'r',

size = 14)

plt.grid(alpha=0.2)

plt.show();

# Create a prophet model without training

def create_model(self):

# Make the model

model = prophet.Prophet(daily_seasonality=self.daily_seasonality,

weekly_seasonality=self.weekly_seasonality,

yearly_seasonality=self.yearly_seasonality,

changepoint_prior_scale=self.changepoint_prior_scale,

changepoints=self.changepoints)

if self.monthly_seasonality:

# Add monthly seasonality

model.add_seasonality(name = 'monthly', period = 30.5, fourier_order = 5)

return model

# Graph the effects of altering the changepoint prior scale (cps)

def changepoint_prior_analysis(self, changepoint_priors=[0.001, 0.05, 0.1, 0.2], colors=['b', 'r', 'grey', 'gold']):

# Training and plotting with specified years of data

train = self.stock[(self.stock['Date'] > (max(self.stock['Date']

) - pd.DateOffset(years=self.training_years)))]

# Iterate through all the changepoints and make models

for i, prior in enumerate(changepoint_priors):

# Select the changepoint

self.changepoint_prior_scale = prior

# Create and train a model with the specified cps

model = self.create_model()

model.fit(train)

future = model.make_future_dataframe(periods=180, freq='D')

# Make a dataframe to hold predictions

if i == 0:

predictions = future.copy()

future = model.predict(future)

# Fill in prediction dataframe

predictions['%.3f_yhat_upper' % prior] = future['yhat_upper']

predictions['%.3f_yhat_lower' % prior] = future['yhat_lower']

predictions['%.3f_yhat' % prior] = future['yhat']

# Remove the weekends

predictions = self.remove_weekends(predictions)

# Plot set-up

self.reset_plot()

plt.style.use('fivethirtyeight')

fig, ax = plt.subplots(1, 1)

# Actual observations

ax.plot(train['ds'], train['y'], 'ko', ms = 4, label = 'Observations')

color_dict = {prior: color for prior, color in zip(changepoint_priors, colors)}

# Plot each of the changepoint predictions

for prior in changepoint_priors:

# Plot the predictions themselves

ax.plot(predictions['ds'], predictions['%.3f_yhat' % prior], linewidth = 1.2,

color = color_dict[prior], label = '%.3f prior scale' % prior)

# Plot the uncertainty interval

ax.fill_between(predictions['ds'].dt.to_pydatetime(), predictions['%.3f_yhat_upper' % prior],

predictions['%.3f_yhat_lower' % prior], facecolor = color_dict[prior],

alpha = 0.3, edgecolor = 'k', linewidth = 0.6)

# Plot labels

plt.legend(loc = 2, prop={'size': 10})

plt.xlabel('Date'); plt.ylabel('Stock Price ($)'); plt.title('Effect of Changepoint Prior Scale');

plt.show()

# Basic prophet model for specified number of days

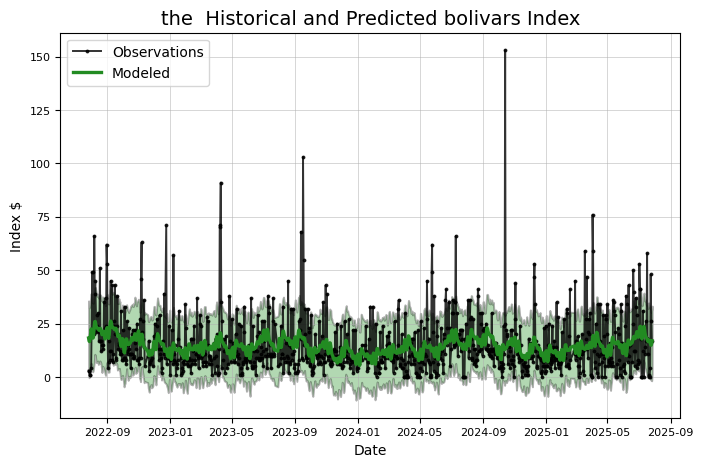

def create_prophet_model(self, days=0, resample=False):

self.reset_plot()

model = self.create_model()

# Fit on the stock history for self.training_years number of years

stock_history = self.stock[self.stock['Date'] > (self.max_date -

pd.DateOffset(years = self.training_years))]

if resample:

stock_history = self.resample(stock_history)

model.fit(stock_history)

# Make and predict for next year with future dataframe

future = model.make_future_dataframe(periods = days, freq='D')

future = model.predict(future)

if days > 0:

# Print the predicted price

predicted_date = future['ds'].iloc[-1]

predicted_value = future['yhat'].iloc[-1]

print('Predicted Index on {} = ${:.2f}'.format(predicted_date, predicted_value))

title = '%s Historical and Predicted bolivars Index' % self.symbol

else:

title = '%s Historical and Modeled bolivars Index' % self.symbol

# Set up the plot

fig, ax = plt.subplots(1, 1)

# Plot the actual values

ax.plot(stock_history['ds'], stock_history['y'], 'ko-', linewidth = 1.4, alpha = 0.8, ms = 1.8, label = 'Observations')

# Plot the predicted values

ax.plot(future['ds'], future['yhat'], 'forestgreen',linewidth = 2.4, label = 'Modeled');

# Plot the uncertainty interval as ribbon

ax.fill_between(np.array(future['ds'].dt.to_pydatetime()),

future['yhat_upper'],

future['yhat_lower'],

alpha=0.3, facecolor='g', edgecolor='k', linewidth=1.4)

# Plot formatting

plt.legend(loc = 2, prop={'size': 10}); plt.xlabel('Date'); plt.ylabel('Index $');

plt.grid(linewidth=0.6, alpha = 0.6)

plt.title(title);

plt.show()

return model, future

# Evaluate prediction model for one year

def evaluate_prediction(self, start_date=None, end_date=None, nshares = None):

# Default start date is one year before end of data

# Default end date is end date of data

if start_date is None:

start_date = self.max_date - pd.DateOffset(years=1)

if end_date is None:

end_date = self.max_date

start_date, end_date = self.handle_dates(start_date, end_date)

# Training data starts self.training_years years before start date and goes up to start date

train = self.stock[(self.stock['Date'] < start_date) &

(self.stock['Date'] > (start_date - pd.DateOffset(years=self.training_years)))]

# Testing data is specified in the range

test = self.stock[(self.stock['Date'] >= start_date) & (self.stock['Date'] <= end_date)]

# Create and train the model

model = self.create_model()

model.fit(train)

# Make a future dataframe and predictions

future = model.make_future_dataframe(periods = 365, freq='D')

future = model.predict(future)

# Merge predictions with the known values

test = pd.merge(test, future, on = 'ds', how = 'inner')

train = pd.merge(train, future, on = 'ds', how = 'inner')

# Calculate the differences between consecutive measurements

test['pred_diff'] = test['yhat'].diff()

test['real_diff'] = test['y'].diff()

# Correct is when we predicted the correct direction

test['correct'] = (np.sign(test['pred_diff']) == np.sign(test['real_diff'])) * 1

# Accuracy when we predict increase and decrease

increase_accuracy = 100 * np.mean(test[test['pred_diff'] > 0]['correct'])

decrease_accuracy = 100 * np.mean(test[test['pred_diff'] < 0]['correct'])

# Calculate mean absolute error

test_errors = abs(test['y'] - test['yhat'])

test_mean_error = np.mean(test_errors)

train_errors = abs(train['y'] - train['yhat'])

train_mean_error = np.mean(train_errors)

# Calculate percentage of time actual value within prediction range

test['in_range'] = False

for i in test.index:

if (test['y'].iloc[i] < test['yhat_upper'].iloc[i]) & (test['y'].iloc[i] > test['yhat_lower'].iloc[i]):

test['in_range'].iloc[i] = True

in_range_accuracy = 100 * np.mean(test['in_range'])

if not nshares:

# Date range of predictions

print('\nPrediction Range: {} to {}.'.format(start_date,

end_date))

# Final prediction vs actual value

print('\nPredicted price on {} = ${:.2f}.'.format(max(future['ds']), future['yhat'].iloc[len(future) - 1]))

print('Actual price on {} = ${:.2f}.\n'.format(max(test['ds']), test['y'].iloc[len(test) - 1]))

print('Average Absolute Error on Training Data = ${:.2f}.'.format(train_mean_error))

print('Average Absolute Error on Testing Data = ${:.2f}.\n'.format(test_mean_error))

# Direction accuracy

print('When the model predicted an increase, the price increased {:.2f}% of the time.'.format(increase_accuracy))

print('When the model predicted a decrease, the price decreased {:.2f}% of the time.\n'.format(decrease_accuracy))

print('The actual value was within the {:d}% confidence interval {:.2f}% of the time.'.format(int(100 * model.interval_width), in_range_accuracy))

# Reset the plot

self.reset_plot()

# Set up the plot

fig, ax = plt.subplots(1, 1)

# Plot the actual values

ax.plot(train['ds'], train['y'], 'ko-', linewidth = 1.4, alpha = 0.8, ms = 1.8, label = 'Observations')

ax.plot(test['ds'], test['y'], 'ko-', linewidth = 1.4, alpha = 0.8, ms = 1.8, label = 'Observations')

# Plot the predicted values

ax.plot(future['ds'], future['yhat'], 'navy', linewidth = 2.4, label = 'Predicted');

# Plot the uncertainty interval as ribbon

ax.fill_between(future['ds'].dt.to_pydatetime(), future['yhat_upper'], future['yhat_lower'], alpha = 0.6,

facecolor = 'gold', edgecolor = 'k', linewidth = 1.4, label = 'Confidence Interval')

# Put a vertical line at the start of predictions

plt.vlines(x=min(test['ds']), ymin=min(future['yhat_lower']), ymax=max(future['yhat_upper']), colors = 'r',

linestyles='dashed', label = 'Prediction Start')

# Plot formatting

plt.legend(loc = 2, prop={'size': 8}); plt.xlabel('Date'); plt.ylabel('Price $');

plt.grid(linewidth=0.6, alpha = 0.6)

plt.title('{} Model Evaluation from {} to {}.'.format(self.symbol,

start_date, end_date));

plt.show();

# If a number of shares is specified, play the game

elif nshares:

# Only playing the stocks when we predict the stock will increase

test_pred_increase = test[test['pred_diff'] > 0]

test_pred_increase.reset_index(inplace=True)

prediction_profit = []

# Iterate through all the predictions and calculate profit from playing

for i, correct in enumerate(test_pred_increase['correct']):

# If we predicted up and the price goes up, we gain the difference

if correct == 1:

prediction_profit.append(nshares * test_pred_increase['real_diff'].iloc[i])

# If we predicted up and the price goes down, we lose the difference

else:

prediction_profit.append(nshares * test_pred_increase['real_diff'].iloc[i])

test_pred_increase['pred_profit'] = prediction_profit

# Put the profit into the test dataframe

test = pd.merge(test, test_pred_increase[['ds', 'pred_profit']], on = 'ds', how = 'left')

test['pred_profit'].iloc[0] = 0

# Profit for either method at all dates

test['pred_profit'] = test['pred_profit'].cumsum().ffill()

test['hold_profit'] = nshares * (test['y'] - float(test['y'].iloc[0]))

# Display information

print('You played the stock market in {} from {} to {} with {} shares.\n'.format(

self.symbol, start_date, end_date, nshares))

print('When the model predicted an increase, the price increased {:.2f}% of the time.'.format(increase_accuracy))

print('When the model predicted a decrease, the price decreased {:.2f}% of the time.\n'.format(decrease_accuracy))

# Display some friendly information about the perils of playing the stock market

print('The total profit using the Prophet model = ${:.2f}.'.format(np.sum(prediction_profit)))

print('The Buy and Hold strategy profit = ${:.2f}.'.format(float(test['hold_profit'].iloc[len(test) - 1])))

print('\nThanks for playing the stock market!\n')

# Plot the predicted and actual profits over time

self.reset_plot()

# Final profit and final smart used for locating text

final_profit = test['pred_profit'].iloc[len(test) - 1]

final_smart = test['hold_profit'].iloc[len(test) - 1]

# text location

last_date = test['ds'].iloc[len(test) - 1]

text_location = (last_date - pd.DateOffset(months = 1))

plt.style.use('dark_background')

# Plot smart profits

plt.plot(test['ds'], test['hold_profit'], 'b',

linewidth = 1.8, label = 'Buy and Hold Strategy')

# Plot prediction profits

plt.plot(test['ds'], test['pred_profit'],

color = 'g' if final_profit > 0 else 'r',

linewidth = 1.8, label = 'Prediction Strategy')

# Display final values on graph

plt.text(x = text_location,

y = final_profit + (final_profit / 40),

s = '$%d' % final_profit,

color = 'g' if final_profit > 0 else 'r',

size = 18)

plt.text(x = text_location,

y = final_smart + (final_smart / 40),

s = '$%d' % final_smart,

color = 'g' if final_smart > 0 else 'r',

size = 18);

# Plot formatting

plt.ylabel('Profit (US $)'); plt.xlabel('Date');

plt.title('Predicted versus Buy and Hold Profits');

plt.legend(loc = 2, prop={'size': 10});

plt.grid(alpha=0.2);

plt.show()

def retrieve_google_trends(self, search, date_range):

# Set up the trend fetching object

pytrends = TrendReq(hl='en-US', tz=360)

kw_list = [search]

try:

# Create the search object

pytrends.build_payload(kw_list, cat=0, timeframe=date_range[0], geo='', gprop='news')

# Retrieve the interest over time

trends = pytrends.interest_over_time()

related_queries = pytrends.related_queries()

except Exception as e:

print('\nGoogle Search Trend retrieval failed.')

print(e)

return

return trends, related_queries

def changepoint_date_analysis(self, search=None):

self.reset_plot()

model = self.create_model()

# Use past self.training_years years of data

train = self.stock[self.stock['Date'] > (self.max_date - pd.DateOffset(years = self.training_years))]

model.fit(train)

# Predictions of the training data (no future periods)

future = model.make_future_dataframe(periods=0, freq='D')

future = model.predict(future)

train = pd.merge(train, future[['ds', 'yhat']], on = 'ds', how = 'inner')

changepoints = model.changepoints

train = train.reset_index(drop=True)

# Create dataframe of only changepoints

change_indices = []

for changepoint in (changepoints):

change_indices.append(train[train['ds'] == changepoint].index[0])

c_data = train.iloc[change_indices, :]

deltas = model.params['delta'][0]

c_data['delta'] = deltas

c_data['abs_delta'] = abs(c_data['delta'])

# Sort the values by maximum change

c_data = c_data.sort_values(by='abs_delta', ascending=False)

# Limit to 10 largest changepoints

c_data = c_data[:10]

# Separate into negative and positive changepoints

cpos_data = c_data[c_data['delta'] > 0]

cneg_data = c_data[c_data['delta'] < 0]

# Changepoints and data

if not search:

print('\nChangepoints sorted by slope rate of change (2nd derivative):\n')

print(c_data[['Date', 'Adj. Close', 'delta']][:5])

# Line plot showing actual values, estimated values, and changepoints

self.reset_plot()

# Set up line plot

plt.plot(train['ds'], train['y'], 'ko', ms = 4, label = 'Stock Price')

plt.plot(future['ds'], future['yhat'], color = 'navy', linewidth = 2.0, label = 'Modeled')

# Changepoints as vertical lines

plt.vlines(cpos_data['ds'].dt.to_pydatetime(), ymin = min(train['y']), ymax = max(train['y']),

linestyles='dashed', color = 'r',

linewidth= 1.2, label='Negative Changepoints')

plt.vlines(cneg_data['ds'].dt.to_pydatetime(), ymin = min(train['y']), ymax = max(train['y']),

linestyles='dashed', color = 'darkgreen',

linewidth= 1.2, label='Positive Changepoints')

plt.legend(prop={'size':10});

plt.xlabel('Date'); plt.ylabel('Price ($)'); plt.title('Stock Price with Changepoints')

plt.show()

# Search for search term in google news

# Show related queries, rising related queries

# Graph changepoints, search frequency, stock price

if search:

date_range = ['%s %s' % (str(min(train['Date'])), str(max(train['Date'])))]

# Get the Google Trends for specified terms and join to training dataframe

trends, related_queries = self.retrieve_google_trends(search, date_range)

if (trends is None) or (related_queries is None):

print('No search trends found for %s' % search)

return

print('\n Top Related Queries: \n')

print(related_queries[search]['top'].head())

print('\n Rising Related Queries: \n')

print(related_queries[search]['rising'].head())

# Upsample the data for joining with training data

trends = trends.resample('D')

trends = trends.reset_index(level=0)

trends = trends.rename(columns={'date': 'ds', search: 'freq'})

# Interpolate the frequency

trends['freq'] = trends['freq'].interpolate()

# Merge with the training data

train = pd.merge(train, trends, on = 'ds', how = 'inner')

# Normalize values

train['y_norm'] = train['y'] / max(train['y'])

train['freq_norm'] = train['freq'] / max(train['freq'])

self.reset_plot()

# Plot the normalized stock price and normalize search frequency

plt.plot(train['ds'], train['y_norm'], 'k-', label = 'Stock Price')

plt.plot(train['ds'], train['freq_norm'], color='goldenrod', label = 'Search Frequency')

# Changepoints as vertical lines

plt.vlines(cpos_data['ds'].dt.to_pydatetime(), ymin = 0, ymax = 1,

linestyles='dashed', color = 'r',

linewidth= 1.2, label='Negative Changepoints')

plt.vlines(cneg_data['ds'].dt.to_pydatetime(), ymin = 0, ymax = 1,

linestyles='dashed', color = 'darkgreen',

linewidth= 1.2, label='Positive Changepoints')

# Plot formatting

plt.legend(prop={'size': 10})

plt.xlabel('Date'); plt.ylabel('Normalized Values'); plt.title('%s Stock Price and Search Frequency for %s' % (self.symbol, search))

plt.show()

# Predict the future price for a given range of days

def predict_future(self, days=30):

# Use past self.training_years years for training

train = self.stock[self.stock['Date'] > (max(self.stock['Date']

) - pd.DateOffset(years=self.training_years))]

model = self.create_model()

model.fit(train)

# Future dataframe with specified number of days to predict

future = model.make_future_dataframe(periods=days, freq='D')

future = model.predict(future)

# Only concerned with future dates

future = future[future['ds'] >= max(self.stock['Date'])]

# Remove the weekends

future = self.remove_weekends(future)

# Calculate whether increase or not

future['diff'] = future['yhat'].diff()

future = future.dropna()

# Find the prediction direction and create separate dataframes

future['direction'] = (future['diff'] > 0) * 1

# Rename the columns for presentation

future = future.rename(columns={'ds': 'Date', 'yhat': 'estimate', 'diff': 'change',

'yhat_upper': 'upper', 'yhat_lower': 'lower'})

future_increase = future[future['direction'] == 1]

future_decrease = future[future['direction'] == 0]

# Print out the dates

print('\nPredicted Increase: \n')

print(future_increase[['Date', 'estimate', 'change', 'upper', 'lower']])

print('\nPredicted Decrease: \n')

print(future_decrease[['Date', 'estimate', 'change', 'upper', 'lower']])

self.reset_plot()

# Set up plot

plt.style.use('fivethirtyeight')

matplotlib.rcParams['axes.labelsize'] = 10

matplotlib.rcParams['xtick.labelsize'] = 8

matplotlib.rcParams['ytick.labelsize'] = 8

matplotlib.rcParams['axes.titlesize'] = 12

# Plot the predictions and indicate if increase or decrease

fig, ax = plt.subplots(1, 1, figsize=(8, 6))

# Plot the estimates

ax.plot(future_increase['Date'], future_increase['estimate'], 'g^', ms = 12, label = 'Pred. Increase')

ax.plot(future_decrease['Date'], future_decrease['estimate'], 'rv', ms = 12, label = 'Pred. Decrease')

# Plot errorbars

ax.errorbar(future['Date'].dt.to_pydatetime(), future['estimate'],

yerr = future['upper'] - future['lower'],

capthick=1.4, color = 'k',linewidth = 2,

ecolor='darkblue', capsize = 4, elinewidth = 1, label = 'Pred with Range')

# Plot formatting

plt.legend(loc = 2, prop={'size': 10});

plt.xticks(rotation = '45')

plt.ylabel('Predicted Price (US $)');

plt.xlabel('Date'); plt.title('Predictions for %s' % self.symbol);

plt.show()

def changepoint_prior_validation(self, start_date=None, end_date=None,changepoint_priors = [0.001, 0.05, 0.1, 0.2]):

# Default start date is two years before end of data

# Default end date is one year before end of data

if start_date is None:

start_date = self.max_date - pd.DateOffset(years=2)

if end_date is None:

end_date = self.max_date - pd.DateOffset(years=1)

# Convert to pandas datetime for indexing dataframe

start_date = pd.to_datetime(start_date)

end_date = pd.to_datetime(end_date)

start_date, end_date = self.handle_dates(start_date, end_date)

# Select self.training_years number of years

train = self.stock[(self.stock['Date'] > (start_date - pd.DateOffset(years=self.training_years))) &

(self.stock['Date'] < start_date)]

# Testing data is specified by range

test = self.stock[(self.stock['Date'] >= start_date) & (self.stock['Date'] <= end_date)]

eval_days = (max(test['Date']) - min(test['Date'])).days

results = pd.DataFrame(0, index = list(range(len(changepoint_priors))),

columns = ['cps', 'train_err', 'train_range', 'test_err', 'test_range'])

print('\nValidation Range {} to {}.\n'.format(min(test['Date']),

max(test['Date'])))

# Iterate through all the changepoints and make models

for i, prior in enumerate(changepoint_priors):

results['cps'].iloc[i] = prior

# Select the changepoint

self.changepoint_prior_scale = prior

# Create and train a model with the specified cps

model = self.create_model()

model.fit(train)

future = model.make_future_dataframe(periods=eval_days, freq='D')

future = model.predict(future)

# Training results and metrics

train_results = pd.merge(train, future[['ds', 'yhat', 'yhat_upper', 'yhat_lower']], on = 'ds', how = 'inner')

avg_train_error = np.mean(abs(train_results['y'] - train_results['yhat']))

avg_train_uncertainty = np.mean(abs(train_results['yhat_upper'] - train_results['yhat_lower']))

results['train_err'].iloc[i] = avg_train_error

results['train_range'].iloc[i] = avg_train_uncertainty

# Testing results and metrics

test_results = pd.merge(test, future[['ds', 'yhat', 'yhat_upper', 'yhat_lower']], on = 'ds', how = 'inner')

avg_test_error = np.mean(abs(test_results['y'] - test_results['yhat']))

avg_test_uncertainty = np.mean(abs(test_results['yhat_upper'] - test_results['yhat_lower']))

results['test_err'].iloc[i] = avg_test_error

results['test_range'].iloc[i] = avg_test_uncertainty

print(results)

# Plot of training and testing average errors

self.reset_plot()

plt.plot(results['cps'], results['train_err'], 'bo-', ms = 8, label = 'Train Error')

plt.plot(results['cps'], results['test_err'], 'r*-', ms = 8, label = 'Test Error')

plt.xlabel('Changepoint Prior Scale'); plt.ylabel('Avg. Absolute Error ($)');

plt.title('Training and Testing Curves as Function of CPS')

plt.grid(color='k', alpha=0.3)

plt.xticks(results['cps'], results['cps'])

plt.legend(prop={'size':10})

plt.show();

# Plot of training and testing average uncertainty

self.reset_plot()

plt.plot(results['cps'], results['train_range'], 'bo-', ms = 8, label = 'Train Range')

plt.plot(results['cps'], results['test_range'], 'r*-', ms = 8, label = 'Test Range')

plt.xlabel('Changepoint Prior Scale'); plt.ylabel('Avg. Uncertainty ($)');

plt.title('Uncertainty in Estimate as Function of CPS')

plt.grid(color='k', alpha=0.3)

plt.xticks(results['cps'], results['cps'])

plt.legend(prop={'size':10})

plt.show();

import pandas as pd

# 讀入資料

df = pd.read_csv('/content/DEXVZUS_out.csv', index_col='ds', parse_dates=['ds'])

# 先用中位數補齊 NaN(每欄各自補自己的中位數)

df_filled = df.fillna(df.median(numeric_only=True))

# 再執行 squeeze(若只有一欄,才會變成 Series)

price = df_filled.squeeze()

# 檢查結果

print(price.tail())

DEXVZUS= Stocker(price)

model, model_data = DEXVZUS.create_prophet_model(days=1 )

import numpy as np

import pandas as pd

from sklearn.preprocessing import MinMaxScaler

from tensorflow.keras.models import Sequential

from tensorflow.keras.layers import LSTM, Dense, Dropout

import matplotlib.pyplot as plt

import matplotlib.dates as mdates

# Prepare data

df = pd.read_csv('output.csv') # Replace with your actual data loading method

df['DATE'] = pd.to_datetime(df['DATE'])

df = df.rename(columns={'DATE': 'date', 'value': 'value'})

# Create lag features (滯後特徵)

def create_lag_features(data, lag=1):

lagged_data = data.copy()

for i in range(1, lag+1):

lagged_data[f'lag_{i}'] = lagged_data['value'].shift(i)

return lagged_data.dropna()

# Create lag features (加入前幾天的價格)

lag = 3 # Use last 3 days to predict

df_lagged = create_lag_features(df, lag)

# Scale the data

scaler = MinMaxScaler()

values_scaled = scaler.fit_transform(df_lagged['value'].values.reshape(-1, 1))

# Create sequences for LSTM

def create_sequences(data, seq_length):

X, y = [], []

for i in range(len(data) - seq_length):

X.append(data[i:(i + seq_length)])

y.append(data[i + seq_length])

return np.array(X), np.array(y)

# Create sequences

seq_length = 12 # Using 12 months of data to predict next month

X, y = create_sequences(values_scaled, seq_length)

# Split data into train and test sets

train_size = int(len(X) * 0.8)

X_train, X_test = X[:train_size], X[train_size:]

y_train, y_test = y[:train_size], y[train_size:]

# Create the LSTM model with modified architecture

model = Sequential([

LSTM(50, return_sequences=True, input_shape=(seq_length, 1)),

Dropout(0.3), # Increased Dropout to avoid overfitting

LSTM(50, return_sequences=False),

Dropout(0.3),

Dense(25, activation='relu'),

Dense(1, activation='relu') # 使用 relu 確保輸出為正數

])

# Compile the model with different optimizer settings

model.compile(optimizer='adam', loss='mse')

# Train the model with more epochs and validation split

history = model.fit(

X_train,

y_train,

epochs=50, # Increased epochs for better training

batch_size=32,

validation_split=0.1,

verbose=1

)

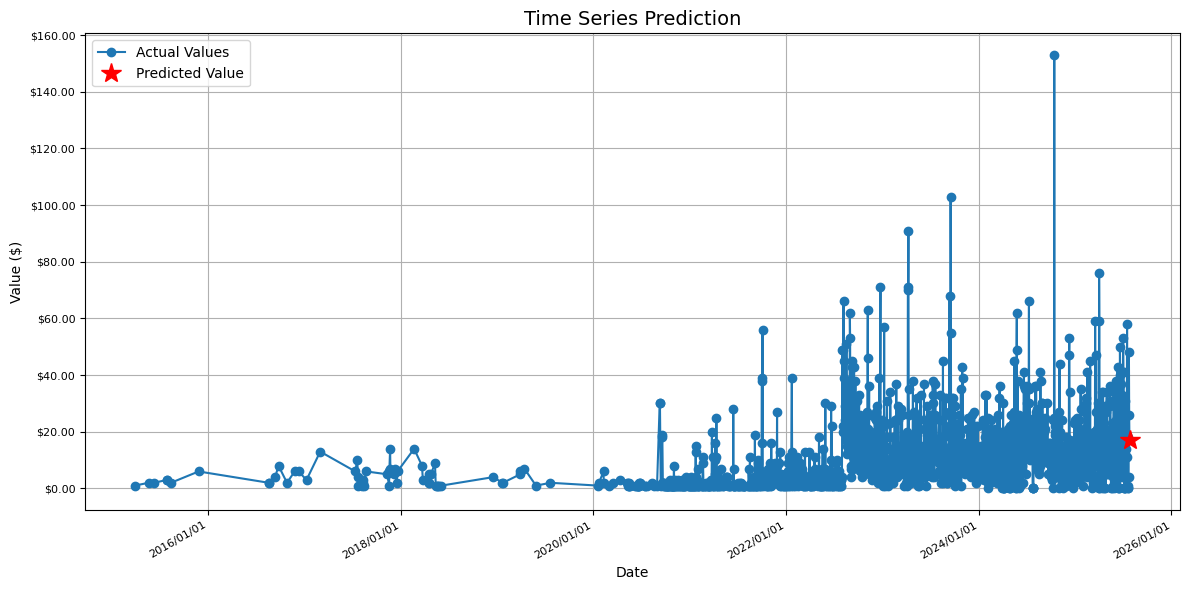

# Predict for 2025/1/8

future_date = pd.Timestamp('2025-07-27')

last_sequence = values_scaled[-seq_length:]

last_sequence = last_sequence.reshape(1, seq_length, 1)

future_pred_scaled = model.predict(last_sequence)

future_pred = scaler.inverse_transform(future_pred_scaled)

print(f'Predicted value for 2025/1/8: ${future_pred[0][0]:,.2f}')

# Plot with enhanced date formatting

plt.figure(figsize=(12, 6))

plt.plot(df['date'], df['value'], label='Actual Values', marker='o')

plt.plot(future_date, future_pred[0][0], 'r*', markersize=15, label='Predicted Value')

# Format x-axis to show dates in YYYY/MM/DD format

plt.gca().xaxis.set_major_formatter(mdates.DateFormatter('%Y/%m/%d'))

plt.gcf().autofmt_xdate() # Rotate and align the tick labels

plt.title('Time Series Prediction')

plt.xlabel('Date')

plt.ylabel('Value ($)')

plt.legend()

plt.grid(True)

# Format y-axis to show dollar values

plt.gca().yaxis.set_major_formatter(plt.FuncFormatter(lambda x, p: f'${x:,.2f}'))

print(f'Predicted value for 2025/1/8: ${future_pred[0][0]:,.2f}')

print(f'Actual value: $369,980.57')

print(f'Absolute error: ${abs(future_pred[0][0] - 369980.57):,.2f}')

print(f'Relative error: {abs(future_pred[0][0] - 369980.57)/369980.57*100:.2f}%')

plt.tight_layout()

plt.show()